Khana Ratsadon and the mission to create a fair tax system in Thai society

Khana Ratsadon and the mission to create a fair tax system in Thai society

After Siam transformed into a democracy, Khana Ratsadon pushed for tax reform to focus on creating a fair tax collection system, emphasizing people's ability to pay taxes.

Taxes have been an important source of revenue for countries since ancient times and have played a crucial role in the formation of many modern states. The same holds true in the context of Thailand, where taxes are an important tool that the state uses to build a modern nation. As a source of revenue for the state, taxes are used to benefit the country by strengthening it at that time.

However, calculating taxes prior to the transition from absolute monarchy to democracy in Thailand had issues with fairness in tax collection. The state's tax collection approach at that time was focused on seeking revenue from the people who earned a living within the country, as if it was seeking protection or tribute, and some types of taxes were levied based on a person's status without considering their ability to pay.

After the transition from absolute monarchy to democracy in Thailand, the condition described above led to the determination of the Khana Ratsadon (the People's Party) to reform the country's tax system with a focus on creating fairness in tax collection, especially by emphasizing people's ability to pay taxes.

When analyzing the causes of unfair tax collection in the past, it is found that it was caused by various factors. However, this article focuses on one specific cause which is the impact that occurred after the signing of the Bowring Treaty between England and Siam or the Bowring Treaty that came to change the economic situation of Siamese society and the determination of tax types, as well as the impact of taxes on society.

The impact of the Bowring Treaty on the economy and taxation system in the past

The Bowring Treaty was a treaty signed between Siam, or Thailand at that time, and Great Britain or the United Kingdom, and Ireland in 1855 AD (2398 BE). One important aspect of this agreement was the issue of taxes and trade, which affected the wealth of Siam.

According to the agreement, Siam was required to abolish port duties and establish clear import and export tax rates. The agreement stipulated a 3% import tax rate for all types of goods, except for opium, which would not be subject to tax but could only be sold to the opium monopoly. For exports, a single tax rate was imposed, and Siam could choose to levy the tax internally (in the form of jungle tax, port tax, or mouth tax) or as an export tax.1

In addition, this treaty also allows English merchants to trade directly with Siamese private businesses without any interference, and the Siamese government must not intervene in such trade activities.2 The result of this treaty was the dismantling of the longstanding monopoly of the royal treasury on trade since the Ayutthaya era3, which had an impact on the revenue of the Siamese government.

In terms of government revenue from taxes, the Bowring Treaty had an impact on the limitations of the Siamese government's revenue expansion at that time, until some parts of the treaty were revised in 1926 (2469 B.E.), allowing the Siamese government to seek revenue to develop industry and the economy to the fullest extent, especially in terms of commercial trade taxes which were relatively limited4.

Looking back at the tax structure as a source of government revenue in Siam during the period of 1855-1925, the main sources of revenue were derived from the specific duty tax and transportation fees, which accounted for 25% of the revenue. The excise tax accounted for 18%, railroad tax for 17%, land tax for 12%, head tax for 10%, and forest and mining taxes for 8% of the budget5.

In addition, prior to the establishment of the Department of Revenue (Hor Ratsadakhon Phiphatsart) during the reign of King Chulalongkorn (around 1874 or 2417 BE), Thailand's tax collection system was based on the "Chao Phaen Nayakorn" system, which made tax collection inefficient and not up to beneficial standards6.

The limitations of taxes resulting from various commercial taxes led the Siamese government to seek other sources of revenue to compensate for the loss of income from state commerce. The emphasis was on collecting taxes from the common people. At that time, tax collection was characterized by redundancy and the collection of various taxes with similar objectives, which imposed a burden on the people and increased the cost of their livelihood.

The tax system in Thai society before the change of governance

Before the Siamese Revolution that changed the form of government to a democracy, the Siamese government collected various direct taxes from the citizens.

An example of taxes during that period was the "Ratchachupakarn tax", which was a direct tax collected from male citizens aged 18-60 years old who were not in military service and not exempted by law7. The Ratchachupopkarn tax differed from the personal income tax for ordinary individuals because it did not rely on the basis of income, property, consumption, or the exploitation of natural resources. Instead, it was collected from the status of individuals as citizens of Siam. It was a form of compensation for the "Prai system" (Prai has the same meaning as peasant) in the past8, and the Ratchachupakarn tax was collected from male citizens at a rate of 4 baht per year, with some regions and periods being taxed as much as 6 baht9.

In terms of unfairness in tax collection, the exemption provisions for the collection of the personal capitation tax create a great deal of injustice for this type of taxpayer. This is because the personal capitation tax has exemptions for individuals with high social status, such as members of the royal family, government officials, soldiers, village chiefs, monks, novices, and students who pass the first or second level of their exams. In addition, the personal capitation tax is exempted for persons with disabilities, Chinese people who have paid poll tax, and those who have just migrated to settle in their first year10.

It can be seen that the main group of taxpayers according to the law are likely to be ordinary citizens who are not government officials and have Thai nationality at that time, mostly farmers, and not wealthy enough to donate money to the government to receive exemptions from paying taxes11. If any citizen does not have money to pay the government, they will have to be forced to work instead of paying taxes12.

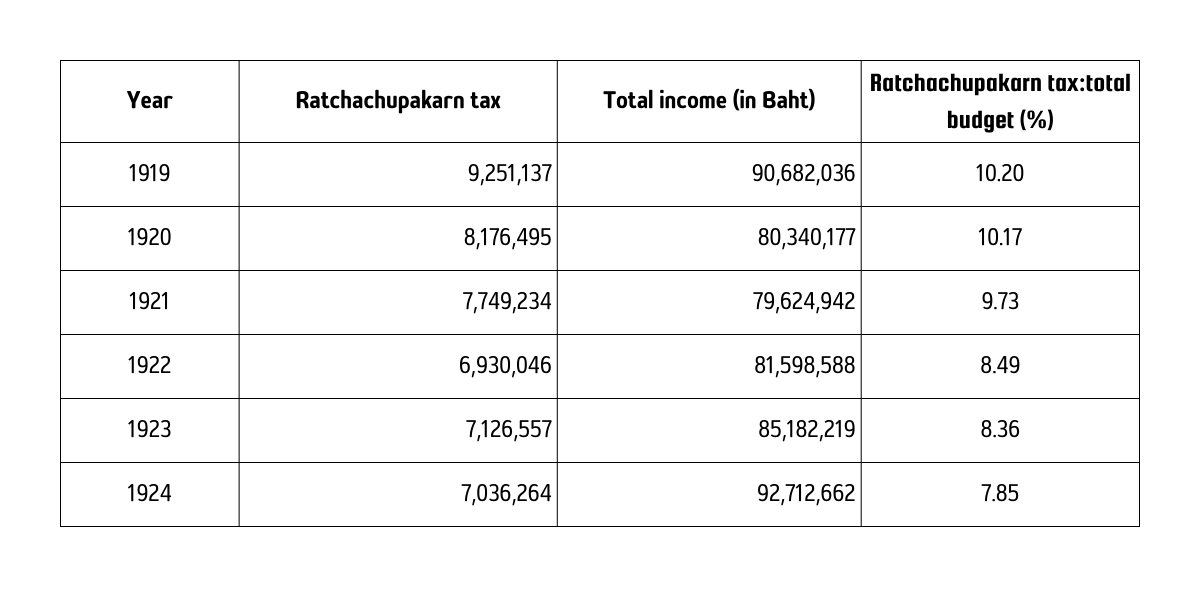

Looking back at the state's revenue collected from royal exemption, it can be seen that the royal exemption provided a significant amount of revenue to the Siamese government. During the period of 1919-1925 (B.E. 2462-2468), it accounted for 7-10% of the government's total revenue.

Table showing statistics of the Ratchachupakarn tax compared to the total income of the country, BE 2462 - 2468 (1919 - 1925)

Source: Somsak Mahatsabsakul, "The Collection of Ratchachupakarn tax and its Impacts on Thai Society, 1901-1939."

Apart from the Ratchachupakarn tax, another type of tax that the government collected heavily at that time was the tax collected from gardens and fields, such as the "Sompatsorn tax" (garden tax), which was the money collected by the government from the area planted with certain types of crops, and the number of certain types of fruit trees (such as jackfruit, longan, pomelo, and tamarind). This tax was collected annually13, or the field tax, garden tax, sugarcane plantation tax, and tobacco tax.

As can be seen, the tax collection system mentioned above is overlapping. That is, the sources of revenue from people's activities come from the same source, but are taxed in many types, especially when it entered the reign of King Rama V. There was an increase in personal income tax collection14.

It was recorded that the difficult living conditions of the people were surveyed by Siam at that time. Carle C. Zimmerman, who was hired by the Siamese government to survey the rural economy in the year 1930, explained that the overlapping and unjust tax system was an additional burden to the people, especially to the farmers who already had low income from their difficult farming. They still had to pay taxes to the government, which made the living conditions of the farmers and rural people more difficult15.

Canceling and improving taxes to make them more fair

After the revolution that changed the government of Siam, the civilian government implemented policies to improve various taxes in order to make them more fair.

The important role in the cancellation and improvement of taxes to be more fair was attributed to Pridi Bhanomyong, in his capacity as the Minister of Finance. He had a policy to abolish unfair taxes16.

The key objective of this tax reform is reflected in the statement made by Direk Jayanama, as a representative of the government, that:

"The government has stated that it will improve taxation to be fair to society...The government adheres to principles that take into account the tax-paying ability of citizens according to their respective income levels, principles of certainty, convenience, and cost-effectiveness, and also considers the political sentiments of the people. The feelings of the people are not only based on the knowledge of a certain class, but have been considered for all levels of society. Whatever is taxed is done so with the hope that those who are able to pay taxes will sacrifice for the prosperity of the nation and the country17."

The intention of tax reform in this instance is for the government to create a new tax system based on the principle of ability to pay of taxpayers. The previous tax system was not based on this principle but rather used taxes to generate wealth for the government. The government aims to consider the ability of taxpayers to pay taxes as a key principle in the new tax system18.

The ultimate result of tax reform by the Khana Ratsadon was the cancellation of overlapping taxes such as the Ratchachupakarn tax, land tax, tree tax, sugarcane tax, and tobacco tax19. At the same time, the government at that time created a new tax system with personal income tax as the centerpiece, which has become the foundation of today's tax system. Tax reform has transformed the new tax system into a principle of "more gain, less pain; less gain, less pain20."

Treaty of Friendship and Commerce between the British Empire and the Kingdom of Siam, Article 8.

Treaty of Friendship and Commerce between the British Empire and the Kingdom of Siam, Article 4.

Khemmapat Trisadikoon, Effects of the Bowring Treaty on the Siamese Economy [Online], 26 July 2021. pridi.or.th/th/content/2021/07/774

Porphant Ouyyanont, A History of Thai Economic Development (Bangkok: Chulalongkorn University Press, 2021), pp. 13-14.

see ibid, pp. 14.

The problem of tax collection is a major and urgent issue, especially in the context of government reform. The establishment of the Revenue Department was aimed at improving tax collection.

Khemmapat Trisadikoon, Revenue Code: Fair Tax System Improvement [Online], 10 October 2020. pridi.or.th/th/content/2020/10/450#_ftn2

Khemmapat Trisadikoon, Ratchachupakarn tax collected from citizen status [Online], 26 October 2520. pridi.or.th/th/content/2020/10/470

Khemmapat Trisadikoon, supra note 7.

The Collecting Civil Servant Money Act, Rattanakosin era 120 (1901), Section 6. The term "Ratchachupakarn tax" used to be referred to as "civil servant money" before it was changed to "Ratchachupakarn tax" later on. However, the exemptions for paying Ratchachupakarn tax have been reduced.

The Collecting Civil Servant Money Act, Rattanakosin era 120 (1901), Section 6.

Khemmapat Trisadikoon, supra note 7.

ibid.

Khemmapat Trisadikoon, supra note 8.

Carle C. Zimmerman, Economic Survey of Rural Siam, translated by Sim Viravaitayai, 2nd edition, (Bangkok: Foundation for Social Sciences and Humanities Textbook Project, 1982), pp. 32.

Sopot Dantakul, Life and Works of Dr. Pridi Bhanomyong, (Bangkok: Sukhapabjai, 2009), pp. 197-198."

Report of the 17th/2481st Meeting of the House of Representatives.

Khemmapat Trisadikoon, supra note 7.

Report of the 17th/2481st Meeting of the House of Representatives.

Sopot Dantakul, supra note 16, pp. 196.